Disclosure: Thank you Capital One for sponsoring this post! This is a paid endorsement. All opinions are my own and were not directed by Capital One. To learn more about Capital One, visit www.capitalonesharemysave.com.

When it comes to collecting items, we all do it. Maybe some more than others, but we’ve all got a few keepsakes that we hold near and dear. It could be school artwork or fun macaroni crafts your child did at school. Maybe it is a collection of baseball cards or dull pennies from decades ago. Me, I like to collect a little bit of everything. My favorite pieces right now are signed footballs from players I once watched.

Passing Down Keepsakes

I would like to think I save my football memorabilia as a piece of history, or a spark in time. I have a small collection of vinyl records and as soon as I place the needle down, I am in another place. It can be a good feeling. What do you save or collect? Could it be jewelry, concert t-shirts, typewriters, stamps, coins, or even old oil cans? Why?

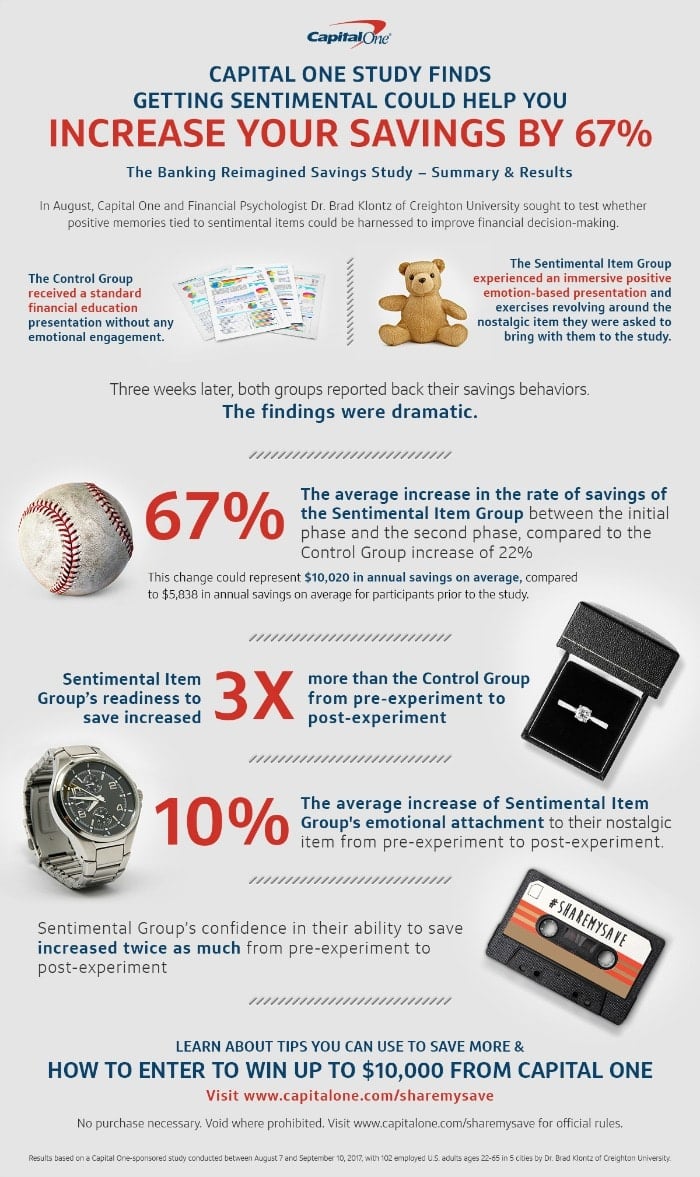

Well, to that point, Capital One recently conducted the Banking Reimagined Sentimental Savings Study in partnership with Financial Psychologist Dr. Brad Klontz and the results are kind of fascinating. They even conducted some of the research right here in our hometown of Dallas! Dr. Klontz of Creighton University sought to test whether positive memories tied to sentimental items, thus powerful and vivid memories, could be harnessed to improve financial decision-making – or, more specifically, savings behavior. The study randomly assigned participants to one of two groups – the control group or the sentimental item group – and compared the results of the two groups. The control group received a standard financial education presentation without any emotional engagement. The sentimental item group experienced an immersive positive emotion-based presentation and exercises revolving around the nostalgic item they were asked to bring with them to the study. Three weeks later, through follow-up with the researchers, the SI group reported back their savings behaviors. The changes were dramatic.

Results From the Sentimental Savings Study

- The sentimental item group increased their savings three times (67%) more than the control group (only 22%) between the initial phase and second phase held three weeks later.

- If maintained over the course of the year, this change could represent $10,020 in annual savings on average, compared to $5,838 in annual savings on average prior to the study.

- Across all five cities, the sentimental item group reported saving, on average, a substantially higher percentage of their gross income three weeks after the emotion-based immersion:

- Boston: 75% increase

- Austin: 40% increase

- Seattle: 47% increase

- Atlanta: 137% increase

- Dallas: 115% increase

The sentimental item group showed statistically significant increases in their financial savings behaviors from pre-experiment to post-experiment: readiness to save, confidence toward saving and financial health.

-

- Readiness to Save: the sentimental item group’s readiness to save increased three times more compared to the control group

- Confidence in Ability to Save More: The sentimental group’s confidence in their ability to save increased twice as much as the control group

- Financial Health: the sentimental group’s reported financial health increased four times more than the control group

Tips and Tricks to Save Money

Most of our financial decisions are not made by our rational brain. They are made by our emotional brain – and our emotional brains are not motivated by numbers or facts. We must engage our emotional brain if we want to change our financial behaviors.

- Get specific. Don’t just have a “savings account.” Name it. Have a “2018 European Family Vacation Account.”

- When you are motivated to take action, automate it!

- For example, set up a monthly contribution from your checking account to a savings account, like Capital One’s 360 Money Market, a high-interest account. It elevates banking as a flexible, fee-free online, mobile and in-person support savings account that offers a rewarding high-interest rate and access to tools needed for long-haul savings growth.

- Come up with an exciting vision of what you are saving for and ask yourself the following questions:

- What would saving for the future get you? What is it you truly want? Get specific. What does it look like? How would it feel to have it? Who might you be enjoy it with? Where are you? What do you see, feel, experience?

- Harness the positive emotion tied to your own sentimental items to improve your savings behavior.

- Think of an item you’ve kept for positive sentimental reasons and ask yourself what kind of feelings and values are associated with that item. Is it something a grandparent or parent gave you and thus is tied to the importance of a loving and supportive family? Or is it something from a vacation abroad that serves as a reminder of a sense of adventure and the great experiences you were lucky to have and that you hope to have more of in the future? Use the power of emotion tied to your sentimental item and the identified feelings and values associated to determine how to live your values today and improve your financial savings behavior.

What Does This Mean to You

- The researchers hypothesize that the sentimental items group were able, through positive, emotionally-charged memories, to develop a deeper emotional incentive for saving money.

- The exercises they engaged in may have enabled them to more viscerally relate saving money to the family, life values and goals that mean the most to them.

- By incorporating sentiment and savings experiences into financial planning -- workshops, money coaching conversations, or even self-directed processes -- It may be possible to successfully harness a person’s emotions in order to facilitate better and healthier financial decision-making.