Having the right type of credit cards can be useful and come with various perks and advantages. It can be overwhelming to choose one credit card when there are so many of them.

While you can't learn everything about each credit card in the world, you may want to know more about the most common types of credit cards to help you decide which credit card will be helpful for your financial needs.

What Types of Credit Cards You Need

It can be hard to select which credit card will work best for you. But if you find a trust credit card to provide financial support for yourself, you can forget about questions such as "is opploans legit and safe" or "where to find money now." Just use your credit cards, and that's all. There are plenty of them on the market today, and each card offers different features.

Each card will have different rewards, interest rates, and annual fees. Check your current credit rating before you opt for a particular Card. This score will tell you where you stand and what cards you can qualify for.

Consumers with excellent and good credit may be eligible for more flexible terms and interest rates. Aim to have your FICO rating of 670 and higher, and don't accumulate too much credit card debt.

Types of Credit Cards Rewards

This card is suitable for consumers who want additional points and cash back. These bonuses will be based on a percentage of the client's spending in popular spending categories such as dining out, gas, or groceries.

These crediting tools offer several ways to redeem the points, such as merchandise, gift cards, and statement credits. You can easily utilize rewards cards for daily costs, provided that you can cover the minimum balance. It offers an opportunity to get travel rewards and cashback for necessary purchases.

Cash Back Credit Cards

This crediting tool works similarly to a rewards card, but it is mainly meant for getting cash back for every dollar a client spends. The card you own may offer various cashback rates in various purchase categories.

Some credit cards offer higher reward rates in particular bonus categories, while others provide a flat rate of cash back on all purchases you make. Most cashback cards don't have an annual fee which is definitely an advantage. However, you will face high-interest rates if you don't pay the minimum monthly balance.

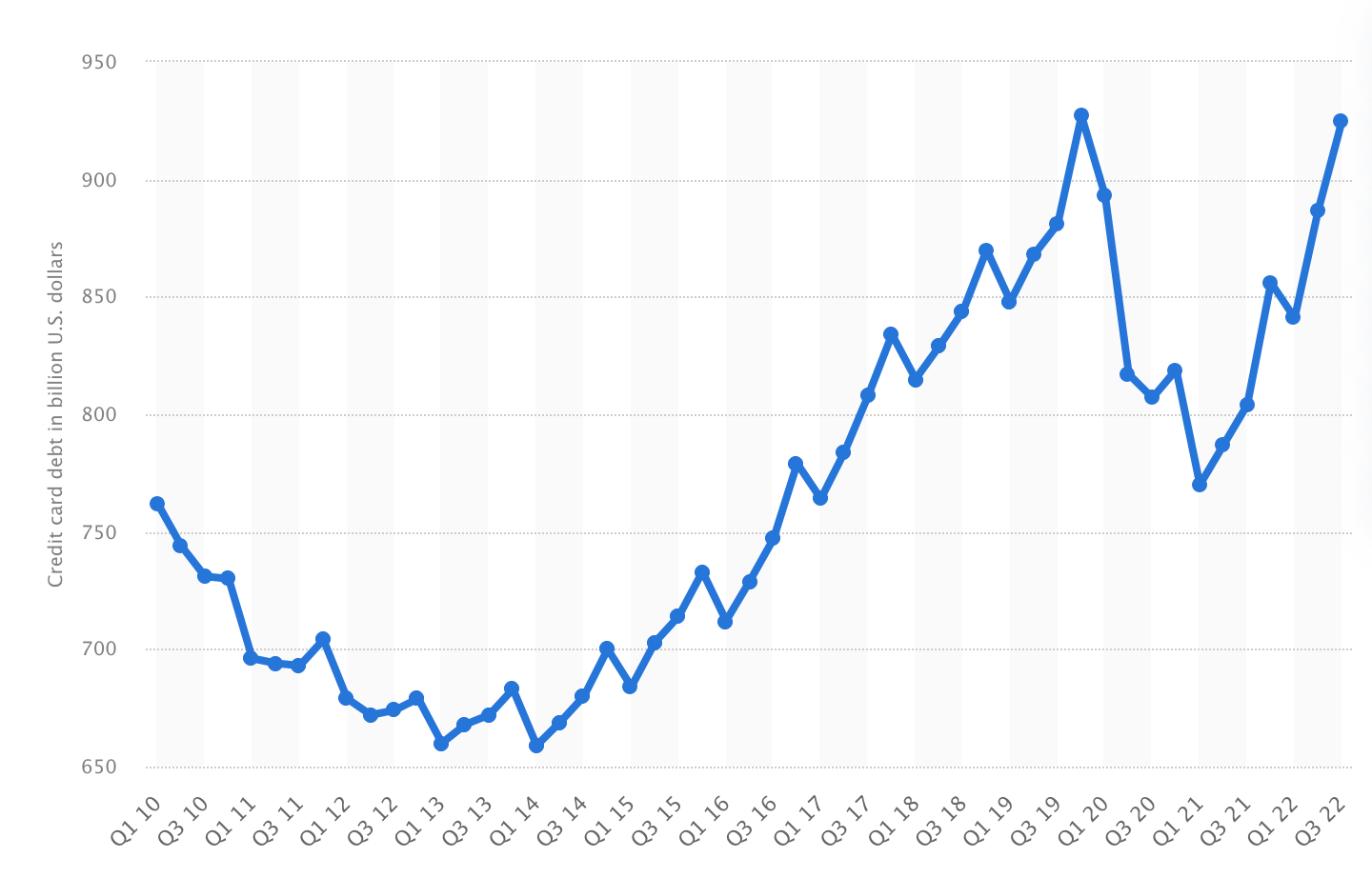

Speaking of the quarterly credit card debt in the USA, it increased by over 40 billion U.S. dollars in the second quarter of 2022 compared to the same quarter of the previous year. The overall credit card debt amounted to 887 billion U.S. dollars in the second quarter of 2022.

Business Credit Cards

Business owners have unique financial needs, so they need to have separate credit cards for their businesses. Such crediting tools come with higher credit lines compared to student cards or general credit card options. Entrepreneurs may enjoy special tracking features for their expenses.

They will be able to customize their spending limits and rewards. How can you obtain a business credit card? You should be the principal or the owner of the venture and be able to provide Employer ID Number (EIN) or Tax ID Number (TIN) together with your personal SSN. Keep in mind that your social security number will be proof that you will be personally accountable for your business credit card debt.

Student Credit Cards

Students belong to a unique group of consumers as their income is very limited while they already have certain monetary needs. What does it mean? It means that students can find rather attractive crediting tools tailored to their financial purposes. The offers can differ in each banking institution and depend on monetary circumstances and overall financial experience.

Such crediting options are suitable for all consumer protections. These cards can often be called starter credit cards, customized for young people with limited credit scores and credit history. Hence, the application isn't tough, and you have a high chance of getting approved.

Secured Credit Cards

The majority of credit cards are unsecured. It means they don't need any guarantee or collateral to secure the funds. Secured crediting tools work best for consumers whose credit rating is below average and who have collateral.

You will be demanded to put down a cash deposit to secure a line of credit. Thus, if you want to obtain a $1,000 line of credit, you will need to sign up for a card and put down a $1,000 initial deposit.

While you may not want to make a deposit, getting approved for a secured credit card will be easier. Such tools are helpful for those who need to build their credit history or repair their rating.

Balance Transfer Cards

These cards are helpful for debt repayment. When you have an existing balance on your card and what to get rid of it, you may opt for a balance transfer card. It usually comes with no APR on balance transfers for up to 21 months.

On the other hand, you will encounter a balance transfer fee. It can range from 3% to 5% of the balance sum transferred. Yet, the long-term interest savings will still be higher compared with this fee. Many balance transfer cards offer continuous rewards and bonuses after the credit card holder pays the balance in full.

Keep in mind that the cards with the longest period of 0% APR may skip these perks. Consumers with a good rating will benefit from using these cards the most and be able to repay existing high-interest debt.

Store Credit Cards

It is another crediting tool offered in retail stores. These cards allow clients to charge the purchases but cover the costs over time. These tools are usually utilized within the particular store that provides them. Certain cards may also be used within some families of stores. Apart from general credit cards, store tools offer higher interest rates.

They can charge deferred interest as well. It means that a consumer gets a 0 or low percent introductory rate for a while but will be charged higher interest if they don't repay the whole sum within this period. Hence, you can benefit from the rewards and bonuses of this card only if you can afford to repay the store credit card balance on time.

Summing Up

To sum up, there are many types of credit cards. You should review each card's bonuses and benefits and select the one that suits your financial needs. Some consumers even have multiple credit cards for various purposes.